Weekly Market Update November 28, 2022

Weekly Market Update November 28, 2022

Presented by Zachary R. Sturdy

General Market News

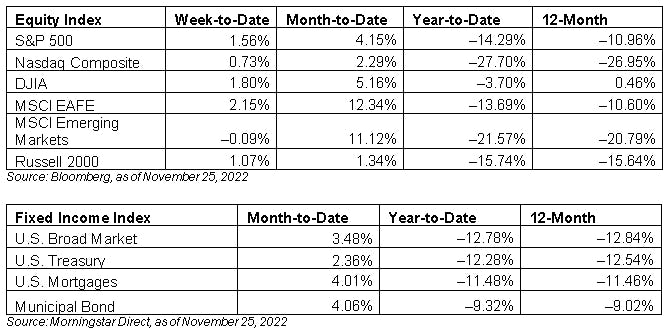

· After the Federal Reserve (Fed)’s fourth consecutive rate increase of 75 basis points (bps), the recently released minutes from the early-November meeting indicate that most Federal Open Market Committee (FOMC) members could support dropping to a smaller rate hike when they reconvene in December. “A substantial majority of participants judged that a slowing in the pace of increase would soon be appropriate,” the minutes read. This comes as inflation remains at a stubbornly high level but is showing signs of potential moderation moving forward. While the pace of ongoing rate hikes is certainly an important piece of the puzzle, market participants are also looking for more clues as to what a likely terminal value may be at the end of the cycle. Currently, expectations are hovering around a terminal rate of about 5 percent, but there is plenty more data to be released before that end point comes more clearly into focus. The U.S. Treasury curve was slightly down last week. The 2-year, 5-year, 10-year, and 30-year lost 2 bps (to 4.5 percent), 3 bps (to 3.92 percent), 4 bps (to 3.73 percent), and 12 bps (to 3.76 percent), respectively.

· Last week’s data was lighter than usual due to the holiday, but the release of durable goods orders and the November FOMC minutes helped provide insight into economic conditions and policy. Equities moved higher as earnings and Fed speak about potentially slower rate increases moving forward helped lift markets. Dell (DELL), HP (HPQ), Analog Devices (ADI), and Deere & Company (DE) all posted modest earnings. While the semiconductor space will take any positive news it can get due to recent headwinds, HP announced it will lay off 6,000 employees through the end of 2025 amid cost cuts. The potential for slower rate increases, however, did not immediately lift growth stocks. The top-performing sectors last week were utilities, materials, financials, and consumer staples. Sectors that underperformed included energy, technology, and consumer discretionary.

· Wednesday saw the preliminary release of durable goods orders for October. Both headline and core durable goods orders came in above expectations during the month, which was a good sign for business spending.

· Wednesday also saw the release of FOMC meeting minutes for November. The minutes from the most recent Fed meeting showed that central bankers are carefully monitoring the path of inflation as they consider slowing the pace of rate hikes at future meetings.

What to Look Forward To

This week’s data will provide a number of insights about consumers, including the November Conference Board’s Consumer Confidence survey and employment report as well as the October income and spending reports.

The week will kick off Tuesday with the Conference Board Consumer Confidence Survey for November. Consumer confidence is set to decline modestly in November, echoing a similar decline in the University of Michigan consumer sentiment survey during the month.

Thursday will see the release of both personal income and spending reports for October and the ISM Manufacturing index for November. Both personal income and personal spending are expected to show continued growth in October. Manufacturing confidence is expected to fall into contractionary territory, highlighting the headwinds that the industry is facing.

Finally, Friday will see the release of the employment report for November. Economists expect to see that 200,000 jobs were added during the month, which would be a step down from the 261,000 that were added in October but still strong on a historical basis.

Disclosures: Certain sections of this commentary contain forward-looking statements that are based on our reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. All indices are unmanaged and are not available for direct investment by the public. Past performance is not indicative of future results. The S&P 500 is based on the average performance of the 500 industrial stocks monitored by Standard & Poor’s. The Nasdaq Composite Index measures the performance of all issues listed in the Nasdaq Stock Market, except for rights, warrants, units, and convertible debentures. The Dow Jones Industrial Average is computed by summing the prices of the stocks of 30 large companies and then dividing that total by an adjusted value, one which has been adjusted over the years to account for the effects of stock splits on the prices of the 30 companies. Dividends are reinvested to reflect the actual performance of the underlying securities. The MSCI EAFE Index is a float-adjusted market capitalization index designed to measure developed market equity performance, excluding the U.S. and Canada. The MSCI Emerging Markets Index is a market capitalization-weighted index composed of companies representative of the market structure of 26 emerging market countries in Europe, Latin America, and the Pacific Basin. The Russell 2000® Index measures the performance of the 2,000 smallest companies in the Russell 3000® Index. The Bloomberg US Aggregate Bond Index is an unmanaged market value-weighted performance benchmark for investment-grade fixed-rate debt issues, including government, corporate, asset-backed, and mortgage-backed securities with maturities of at least one year. The U.S. Treasury Index is based on the auctions of U.S. Treasury bills, or on the U.S. Treasury’s daily yield curve. The Bloomberg US Mortgage Backed Securities (MBS) Index is an unmanaged market value-weighted index of 15- and 30-year fixed-rate securities backed by mortgage pools of the Government National Mortgage Association (GNMA), Federal National Mortgage Association (Fannie Mae), and the Federal Home Loan Mortgage Corporation (FHLMC), and balloon mortgages with fixed-rate coupons. The Bloomberg US Municipal Index includes investment-grade, tax-exempt, and fixed-rate bonds with long-term maturities (greater than 2 years) selected from issues larger than $50 million. One basis point is equal to 1/100th of 1 percent, or 0.01 percent.

###

Zachary R. Sturdy is located at 307 S. Front St., Ste: 107 Marquette MI, 49855 and can be reached at (906)226-6056.

Securities and Advisory Services offered through Commonwealth Financial Network, member FINRA/SIPC, a Registered Investment Adviser. Fixed insurance products and services offered through CES Insurance Agency.

Authored by the Investment Research team at Commonwealth Financial Network.

© 2022 Commonwealth Financial Network®