Weekly Market Update February 13, 2023

Weekly Market Update February 13, 2023

Presented by Zachary R. Sturdy

General Market News

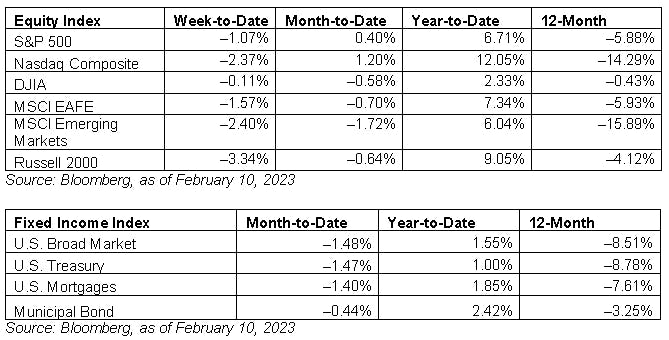

· Rates continued their move higher last week as several Federal Reserve (Fed) members, including Chairs Powell, Kashkari, and Waller indicated there was potentially “more work to do.” U.S. Treasury yields were up last week, with the 2-year, 10-year, and 30-year increasing 42 basis points (bps) (to 4.51 percent), 34 bps (to 3.74 percent), and 30 bps (to 3.82 percent), respectively.

· This year’s rally gave back some of its gains last week. Jerome Powell reiterated his comments from the Federal Open Market Committee (FOMC) meeting last week at the Economic Club of Washington. Powell indicated that while inflation is coming down, inflation likely will not be back near the 2 percent target until next year. This was echoed by the University of Michigan consumer sentiment survey, which found that consumers’ one-year target inflation rate was 4.2 percent, up from 3.9 last month.

· The result was that many of the small-cap and tech names that have rallied hard since November struggled last week. Alphabet, Amazon, Meta Platforms, Netflix, and AMD were all down more than 5 percent. Alphabet’s stock was also down on the news of the Microsoft announcement that artificial intelligence would be incorporated into its Microsoft Edge browser and Bing search engine. Alphabet announced its own artificial intelligence search enhancements to Google. Investors overall preferred to ignore the search and ad space and pivoted to energy, health care, and utilities. Communication services, consumer discretionary, and REITs were among the worst-performing sectors.

· Last week was light on data. Tuesday saw the release of the international trade report for December. The trade deficit widened less than expected in December. Imports increased by 1.3 percent, while exports fell 0.9 percent.

· Friday wrapped with the University of Michigan consumer sentiment survey for January. Consumer sentiment improved more than expected to start the month, driven by improving consumer views on current economic conditions. This better-than-expected result brought the index to its highest level in over a year.

What to Look Forward To

This week will be another busy one in terms of economic data. Tuesday will see the release of the Consumer Price Index report for January. Headline consumer prices are set to rise in January following a modest decline in December. On a year-over-year basis, consumer inflation is expected to decelerate to start the year.

On Wednesday, retail sales, industrial production, and the National Association of Home Builders Housing Market Index are all set to be released. Retail sales are set to rebound in January following a decline in December. Part of the anticipated increase is due to rising gas prices during the month; however, core sales are also expected to grow, indicating healthy levels of consumer demand. Industrial production is expected to improve, supported by rising manufacturing output. Home builder confidence is expected to increase modestly in February following a larger-than-expected increase in January.

Finally, the week will wrap Thursday with the release of housing starts and building permits and the Producer Price Index. Building permits are expected to increase modestly while housing starts are set to decline. Both headline and core producer prices are set to rise in January; however, on a year-over-year basis, both measures of producer inflation are expected to slow.

Disclosures: Certain sections of this commentary contain forward-looking statements that are based on our reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. All indices are unmanaged and are not available for direct investment by the public. Past performance is not indicative of future results. The S&P 500 is based on the average performance of the 500 industrial stocks monitored by Standard & Poor’s. The Nasdaq Composite Index measures the performance of all issues listed in the Nasdaq Stock Market, except for rights, warrants, units, and convertible debentures. The Dow Jones Industrial Average is computed by summing the prices of the stocks of 30 large companies and then dividing that total by an adjusted value, one which has been adjusted over the years to account for the effects of stock splits on the prices of the 30 companies. Dividends are reinvested to reflect the actual performance of the underlying securities. The MSCI EAFE Index is a float-adjusted market capitalization index designed to measure developed market equity performance, excluding the U.S. and Canada. The MSCI Emerging Markets Index is a market capitalization-weighted index composed of companies representative of the market structure of 26 emerging market countries in Europe, Latin America, and the Pacific Basin. The Russell 2000® Index measures the performance of the 2,000 smallest companies in the Russell 3000® Index. The Bloomberg US Aggregate Bond Index is an unmanaged market value-weighted performance benchmark for investment-grade fixed-rate debt issues, including government, corporate, asset-backed, and mortgage-backed securities with maturities of at least one year. The U.S. Treasury Index is based on the auctions of U.S. Treasury bills, or on the U.S. Treasury’s daily yield curve. The Bloomberg US Mortgage Backed Securities (MBS) Index is an unmanaged market value-weighted index of 15- and 30-year fixed-rate securities backed by mortgage pools of the Government National Mortgage Association (GNMA), Federal National Mortgage Association (Fannie Mae), and the Federal Home Loan Mortgage Corporation (FHLMC), and balloon mortgages with fixed-rate coupons. The Bloomberg US Municipal Index includes investment-grade, tax-exempt, and fixed-rate bonds with long-term maturities (greater than 2 years) selected from issues larger than $50 million. One basis point is equal to 1/100th of 1 percent, or 0.01 percent.

###

Zachary R. Sturdy is located at 307 S. Front St., Ste: 107 Marquette MI, 49855 and can be reached at (906)226-6056.

Securities and Advisory Services offered through Commonwealth Financial Network, member FINRA/SIPC, a Registered Investment Adviser. Fixed insurance products and services offered through CES Insurance Agency.

Authored by the Investment Research team at Commonwealth Financial Network.

© 2023 Commonwealth Financial Network®